Life insurance companies are stuck between a rock and a hard place.

On the one hand, there’s a need to drive efficiencies that flow through to value for money from the perspective of advisers and clients. On the other, continued losses in the sector driven in large part by claims on disability income insurance (DII) make this a near-impossible task.

Life companies across the board are being forced to hike premiums to ensure pricing remains sustainable, but if APRA’s life insurance statistics for year-end 2020 are any indication of what’s to come, the premium rises are far from over.

The life sector continues to post large-scale losses. While the net loss after tax of $0.1 billion in the year to December 2020 is a marked improvement over 2019, when the industry suffered a $0.3 billion loss, it’s still a concerning trend that needs to be arrested.

As APRA points out, the main driver of the improvement was a significant release of reserves to offset the investment losses and claims payments shelled out during the year.

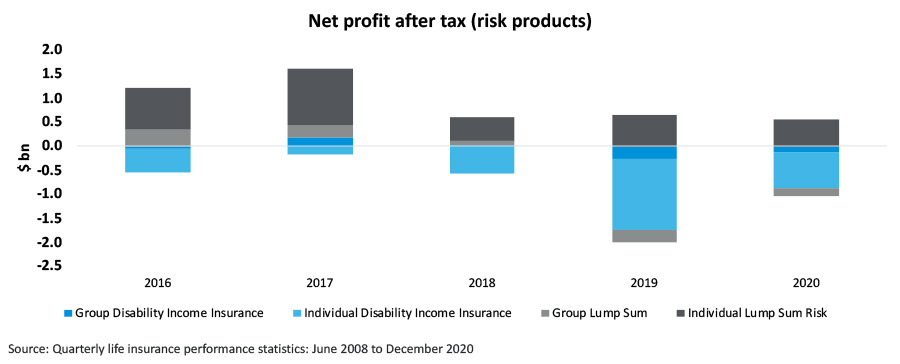

Combined losses

Risk products reported a combined net loss after tax of $492.3 million, with the net profit of $543.7 million on individual lump sum offset by the $739.9 million loss on DII. The 2020 risk result was similarly an improvement over 2019, when the industry haemorrhaged $1.33 billion, but even the one profitable part of the sector – individual lump sum – saw a deterioration in net profit over the year.

In an environment where pricing is converging and products are becoming increasingly homogenised, customer service is the primary way to differentiate.

And CoreData’s latest research among Australian financial planners suggests life companies are performing well in this regard.

Our latest quarterly Adviser Pulse Check of more than 160 advisers found approximately seven in 10 (71.4%) planners offering risk are satisfied with the customer service they receive from their main life company (the one they use most).

While the majority of planners surveyed were satisfied with premium value for money (62.1%), satisfaction with premiums was lower than with the overall adviser experience (72.9%) and adviser communications (70.0%).

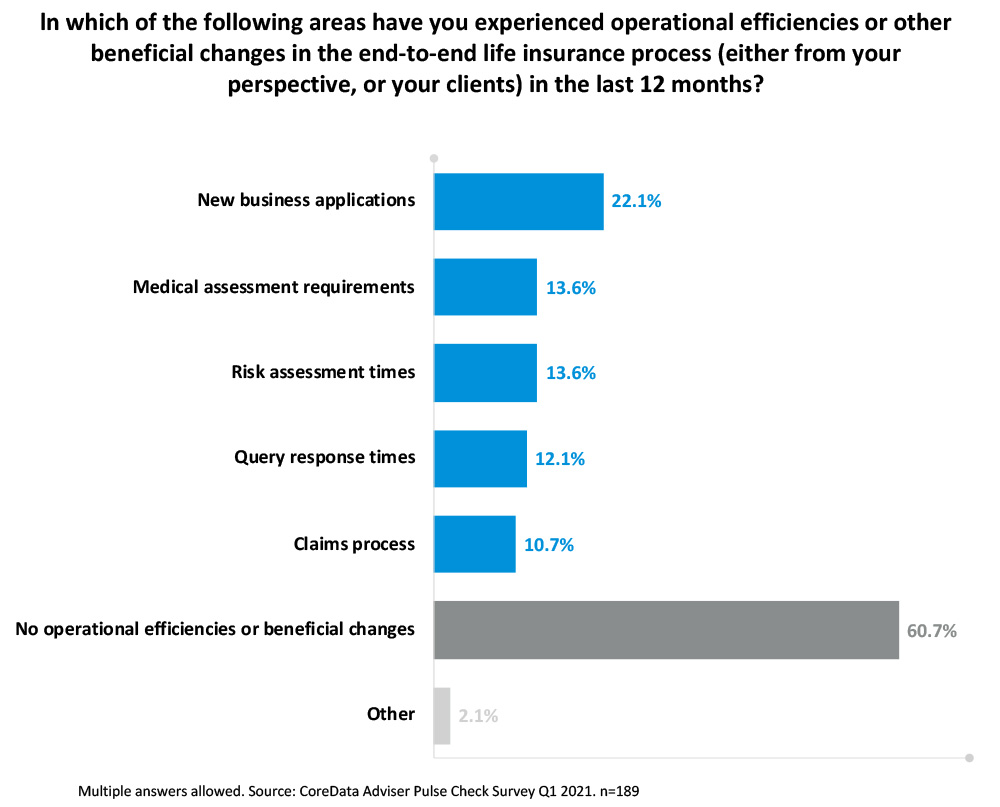

Further, most planners (60.7%) had not experienced any operational efficiencies or other beneficial changes in the end-to-end life insurance process, from either their perspective or that of their clients.

We’ve arguably reached a point whereby the cost of delivering risk advice exceeds the amount clients are willing to pay for that advice. Planners are being forced to reprice services, but in a market where risk continues to be sold not bought, passing the cost of service delivery to the consumer is likely to create even bigger barriers to take up, and see fewer Australians adequately insured.

‘Poor member outcomes’

Pushing everyone into group life insurance is not the answer either. In a letter from APRA to life companies and super funds earlier this month, the regulator foreshadowed ‘poor member outcomes’ if the “re-emergence of some concerning developments in group life insurance in superannuation” were not addressed.

These developments included premium volatility, availability and provision of data, and tender practices.

APRA likened the recent developments to trends in 2012-2016, when insurers experienced significant losses leading to premium increases, more restrictive cover terms and difficulty in obtaining quotes for member cover.

Ensuring the sustainability and affordability of life insurance to everyday Australians requires a multi-pronged approach.

Planners need to find greater efficiencies through technology, life companies need to offer seamless customer service to reduce the time spent by planners delivering risk advice, and clients need to understand the value of the advice so that they’re willing to pay what it’s worth.